Pioneering Sustainable Lithium

Plug into our story: Bridging green energy and pioneering lithium extraction, unleashing innovative technology, and the lithium market.

Introduction to the Sustainable Path Forward

Welcome to Lithium Harvest, where we navigate the journey toward a sustainable energy future. Our current energy landscape is marked by the urgent need to reduce greenhouse gas (GHG) emissions. The legacy of over a century of reliance on fossil fuels has led to a critical juncture; the atmosphere laden with GHGs is altering our climate at an alarming rate. The call for change is clear and unmistakable.

Here, at the forefront of the green energy revolution, we invite you to explore how our commitment to sustainable lithium extraction drives innovation and delivers value. Delve into our strategies, technologies, and market insights that distinguish us as frontrunners in the energy realm. Uncover the expansive potential and impact of the lithium mining industry and engage with us as we endeavor to revolutionize the lithium mining industry.

Our Planet Is Running Low on Battery

The Environmental Challenge: A Call to Action

Our planet faces a defining moment. Despite years of international climate agreements, global greenhouse gas (GHG) emissions have steadily risen since 2000, with only a brief 3.7% dip during the COVID-19 pandemic in 2020. By 2023, emissions surged to a record 53.0 gigatons of CO₂ equivalent (Gt CO₂eq), a 1.9% increase from 2022. This swift rebound underscores the magnitude of the challenge ahead. GHGs trap heat and contribute to the planet’s warming, with human activities driving nearly all atmospheric GHG increases over the last 150 years.

The leading contributors - China, the United States, India, the EU27, Russia, and Brazil - are responsible for 62.7% of global GHG emissions. In 2023, fossil fuel combustion alone accounted for 73.7% of these emissions, underscoring the continued reliance on traditional energy sources. This path has led to a consistent rise in global temperatures, with an increase of 1.36°C (2.45°F) since the late 19th century. The effects are increasingly evident: more frequent extreme weather events, rising sea levels, and disrupted ecosystems.

Science shows that to avoid the most severe impacts of climate change and maintain a habitable planet, we must limit global temperature rises to 1.5°C above pre-industrial levels. To keep global warming to no more than 1.5°C – as called for in the Paris Agreement – emissions need to be reduced by 45% by 2030 and reach net zero by 2050.

Even a one-degree global temperature change is significant. To this extent, an enormous amount of heat is required to warm the oceans, atmosphere, and land masses. Historically, a one- to two-degree drop was enough to trigger the Little Ice Age, while a five-degree drop buried large parts of North America under ice sheets 20,000 years ago. These precedents remind us how delicate our climate is and the pressing need to reverse the current trend.

Greenhouse Gas Emission by Industry

Greenhouse gas emissions permeate through every sector of our economy, with key industries contributing significantly to our environmental footprint. The primary sources are transportation, electric power generation, industry, and the residential and commercial sectors.

-

Transportation

Transportation generated 37% of U.S. GHG emissions in 2023, primarily from fossil fuel combustion in cars, trucks, ships, trains, and planes. Particulate matter (PM) emissions from internal combustion engines (ICE) have been linked to significant health problems, prompting governments to implement regulations to reduce PM emissions. Despite these efforts, economic growth has led to historically high pollution levels in major cities.

Over 94% of the fuel used for transportation is petroleum-based, mainly gasoline and diesel.

-

Electricity Production

The electricity production sector generated 31% of U.S. GHG emissions in 2023 and includes emissions from electricity production used by other end-use sectors (e.g., industry). 79% of our electricity comes from burning fossil fuels, mainly coal and natural gas.

-

Industry

Industrial activities accounted for 13% of U.S. GHG emissions in 2023, primarily coming from burning fossil fuels for energy, as well as GHG emissions from specific chemical reactions necessary to produce goods from raw materials. If emissions from electrical use are allocated to the industrial end-use sector, industrial activities account for a much larger share of U.S. GHG emissions.

-

Commercial & Residential

The commercial and residential sectors contributed 13% of U.S. GHG emissions in 2023, mainly from burning fossil fuels for heat, lighting, and using gases for refrigeration and cooling in businesses and homes, as well as non-building-specific emissions such as waste handling. If emissions from electrical use are allocated to the commercial and residential end-use sectors, commercial and residential activities account for a much larger share of U.S. greenhouse gas emissions.

The Solution to Climate Change

As the world confronts the pressing issue of global warming, two pivotal shifts are at the core of our collective response: the adoption of renewable energy sources and the electrification of transportation. These transformative movements, underpinned by lithium-ion technology, accelerate our departure from fossil fuels and drive a cleaner, more sustainable future.

Accelerating the Shift to Renewable Energy

The key to managing global warming is to limit GHG emissions by transitioning from fossil fuels to intermittent renewable energy sources (IRES), such as wind power, solar power, and hydroelectric power. However, transitioning from fossil fuels to IRES requires efficient energy storage solutions to manage their variability and ensure a consistent energy supply.

Lithium-ion batteries have emerged as the key technology for this transition. They provide a scalable, efficient solution for storing renewable energy, enabling the seamless integration of IRES into the grid. By storing excess energy generated during peak production times and releasing it when demand is high, lithium-ion batteries help stabilize the grid and reduce dependence on fossil fuels.

Electrification of Transportation

The transportation sector is one of the most significant contributors to GHG emissions, accounting for 35% of the U.S. total in 2022. Decarbonizing this sector is crucial to achieving global climate goals. Electric vehicles (EVs) are the key technology to this transformation, and lithium-ion batteries are at the heart of this revolution.

Lithium-ion batteries offer increased energy density, reduced weight, and enhanced performance compared to traditional batteries. These advancements translate into longer driving ranges, faster charging times, and more affordable EVs, making them increasingly attractive to consumers and businesses.

Lithium: The Essential Element for the Solution

Lithium is at the core of the global transition to a low-carbon economy and electrification. As a critical material in lithium-ion batteries, it enables the efficient storage of renewable energy and powers the electrification of transportation. By facilitating the shift from fossil fuels to electrification, lithium is not just a commodity - it is a critical enabler in the fight against climate change.

Global Initiatives & Regulatory Developments

Global initiatives and regulatory frameworks play a crucial role in steering the collective action toward a more sustainable future. These policies and agreements shape the trajectory of industry and consumer behavior, incentivizing progress while establishing benchmarks for success in the transition to greener practices.

-

Global Alliances

A growing coalition of countries, cities, businesses, and other institutions are pledging to get to net-zero emissions. More than 70 countries, including the biggest polluters – China, the United States, and the European Union – have set a net-zero target, covering about 76% of global emissions. More than 3,000 businesses and financial institutions are working with the Science-Based Targets Initiative to reduce their emissions in line with climate science. Over 1000 cities, over 1000 educational institutions, and over 400 financial institutions have joined the Race to Zero, pledging to take rigorous, immediate action to halve global emissions by 2030.

The energy sector is the source of around three-quarters of greenhouse gas emissions today and holds the key to averting the worst effects of climate change. Replacing polluting coal, gas, and oil-fired power with energy from renewable sources, such as wind or solar, would dramatically reduce carbon emissions. This transition can only be achieved by increasing the use of energy storage solutions, such as Lithium-ion batteries, and electrifying transportation.

-

Banning of ICE Vehicles

Vehicles powered by fossil fuels, such as gasoline and diesel, are set to be phased out by several countries.

Many countries and cities worldwide have already stated they will ban the sales of passenger vehicles (primarily cars and buses) powered by fossil fuels at some time in the future.

A few places have also set dates for banning other types of vehicles, such as fossil-fueled ships and lorries.

In addition to these national bans, more than 100 countries, cities,

financial institutions, and multinationals, including Ford Motor Company, General Motors, Volvo Cars, and other automakers, signed the Glasgow Declaration on Zero-Emission Cars and Vans to end the sale of internal combustion engines by 2035 in leading markets, and by 2040 worldwide. -

The Inflation Reduction Act

The Inflation Reduction Act underscores the imperative for the United States to achieve autonomy in lithium production, a critical component of the burgeoning electric vehicle (EV) industry and renewable energy sector. In a significant move to bolster domestic capabilities, the U.S. government unveiled the National Blueprint for Lithium Batteries 2021-2030. This strategic document lays out a comprehensive framework for creating a resilient supply chain for battery materials and technologies within the nation. It aims to encourage EV manufacturers to ramp up production in North America and diversify the sourcing of essential minerals from countries with free-trade agreements with the U.S., thereby reducing reliance on China.

These regulatory measures are reshaping the global supply chain landscape, signaling a shift towards more geographically diversified and secure sources of raw materials. The United States is actively seeking to expand its supply chain development efforts, as evidenced by its negotiations with the European Union (EU) on extending U.S. tax credits. This move aligns with the EU’s pursuit of dependable partners for the supply of raw materials, potentially paving the way for a collaborative EV ecosystem between the U.S. and the EU.

However, the challenge remains formidable, with the current production of Lithium Carbonate Equivalent (LCE) in the U.S. and Europe nearly nonexistent. This scenario indicates a market in transition, with concerted efforts aimed at securing lithium and other vital materials essential for the green energy transition. The strategic response to these developments will be critical in shaping the future of sustainable energy and transportation.

-

The European Critical Raw Material Act

European Union announced the Critical Raw Materials action plan in March 2023.

The Act will reduce the administrative burden and simplify permitting procedures for critical raw materials projects in the EU, Strengthening the uptake and deployment of breakthrough technologies in critical raw materials. However, as the EU accepts that it will never be self-sufficient in supplying such raw materials, it has focused on supporting global production and ensuring supply diversification.

The EU must strengthen its global engagement with reliable partners to develop and diversify investment, promote stability in international trade, and strengthen legal certainty for investors. Additionally, the Act provides for monitoring critical raw materials supply chains to ensure their resilience.

The EU will focus on improving the circularity and sustainability of critical raw materials. A partnership on critical raw materials and a Raw Materials Academy will promote skills relevant to the workforce in critical raw materials supply chains. It will further develop strategic alliances: The EU will work with reliable partners to promote their economic development sustainably through value chain creation in their own countries while also promoting secure, resilient, affordable, and sufficiently diversified value chains for the EU.

-

The European Batteries Regulation

The European Union has initiated a significant regulatory change by introducing the new EU Battery Regulation, which began to apply on 18 February 2024. This regulation represents a landmark move towards more sustainable, circular, and safe battery production and use within the EU. However, it's important to note that the regulation's provisions are not all applied immediately but are introduced in phases over the coming years. This phased approach allows for some aspects of the regulation to become stricter over time, with certain areas of implementation still to be defined.

One of the regulation's critical requirements is that manufacturers and importers of batteries intending to enter the European market must comply with these new standards. Non-compliance could lead to significant penalties, including restricting or withdrawing non-compliant batteries from the market, depending on the enforcement policies of individual EU countries.

Carbon Footprint Disclosure

A cornerstone of the regulation is requiring all batteries to disclose their carbon footprint by 18 February 2025. This disclosure must encompass the entire life cycle of the battery, from the extraction of raw materials and processing to manufacturing and, finally, to the recycling stage. Notably, the use phase of the battery is currently excluded from this requirement. This measure aims to increase transparency and encourage the production of batteries with a lower environmental impact.

Supporting the Green Transition

Batteries are recognized as a crucial technology in driving the green transition, supporting sustainable mobility, and contributing towards the EU's goal of climate neutrality by 2050. In alignment with these objectives, the regulation will gradually introduce declaration requirements, performance classes, and maximum limits on the carbon footprint for various types of batteries. This includes batteries used in electric vehicles, light means of transport such as e-bikes and scooters, and rechargeable industrial batteries, starting from 2025.

The EU Battery Regulation is a significant step forward in ensuring that batteries contribute positively to the green transition and sustainable mobility. By setting stringent requirements for their production, use, and recycling, the EU aims to minimize their environmental impact and pave the way for a climate-neutral future.

Countries are Banning ICE Vehicles

Before 2025 |

Before 2030 |

Before 2035 |

Before 2040 |

|

|---|---|---|---|---|

| Belgium | - | New vehicle sales (2029) | - | - |

| Canada | - | - | New light-duty vehicle sales | - |

| Chile | - | - | New vehicles sales | - |

| China | - | - | New private vehicles sales and registration | - |

| Denmark | - | New vehicles sales | - | - |

| Egypt | - | - | - | New vehicle sales |

| Germany | - | - | New vehicles sales | - |

| Greece | - | New vehicles sales | - | - |

| Iceland | - | New vehicles sales | - | - |

| Italy | - | - | New private vehicles sales | New commercial vehicle sales |

| Japan | - | - | New vehicles sales | - |

| Korea | - | - | New vehicles sales | - |

| Malaysia | - | - | - | New vehicles sales (2050) |

| Netherlands | - | New private vehicle sales | - | New commercial vehicle sales |

| Norway | New private vehicles sales | - | New commercial vehicles sales | - |

| Portugal | - | - | New vehicles sales | - |

| Singapore | New public vehicles (2023), new taxis | New vehicles sales | - | - |

| Sweden | - | New vehicles sales | - | - |

| Taiwan | - | New government-owned vehicles | New motorcycle sales | New vehicle sales |

| United Kingdom | - | - | New light-duty vehicle sales | New heavy-duty vehicle sales |

| United States | - | New government-owned light-duty vehicles (2027) | New government-owned vehicles | - |

Before 2025

Before 2030

Before 2035

Before 2040

The Car Industry Is Moving Toward EVs

The automobile industry is rapidly transitioning towards electric vehicles (EVs) due to increasing consumer demand for eco-friendly and sustainable transportation options. According to IEA, EVs will make up 50% of all cars sold globally in 2035. The global EV fleet is projected to grow twelve-fold to 585 million by 2035, with an average annual growth of 24% from 2023 to 2035. In addition, many governments worldwide are implementing policies to encourage EV use, such as tax incentives, rebates, and subsidies for EV purchases, as well as mandates for automakers to produce more low-emission vehicles.

Major automakers have also announced ambitious plans to transition towards EVs in the coming years, with some companies pledging to phase out the production of gasoline and diesel-powered vehicles altogether. For example, Volvo has committed to producing only electric vehicles by 2030, and General Motors plans to sell only EVs by 2040.

This shift towards electric vehicles marks a significant turning point for the automotive industry as it moves towards a more sustainable and environmentally conscious future.

Before 2030 |

Before 2035 |

Before 2040 |

Before 2050 |

|

|---|---|---|---|---|

| Bentley | Stops ICE vehicle sales shortly after 2030 | - | - | - |

| Volkswagen | Sets goals for 80% EV sales in Europe and 55% in North America | Stops ICE vehicle sales in Europe | - | - |

| Volvo | Fully electric sales | - | - | Completely CO₂ neutral |

| Toyota | 55 electrified models (2025) on sale and 50% ZEV sales | - | - | - |

| Jaguar | Fully electric sales (2025) | - | - | - |

| Mercedes-Benz | 50% electrified sales | - | - | - |

| Subaru | 50% electrified sales | - | - | - |

| Hyundai | - | 100% electrified sales in Europe | Close to 100% electrified global sales | - |

| Nissan | 100% BEV sales in Europe | - | - | - |

| General Motors | - | - | Aims to stop ICE sales | Carbon neutrality across the company's operations and the life cycle of its products |

| Renault | 100% EV sales in Europe | - | - | - |

| Mazda | EVs between 25% and 40% of global sales | - | - | Carbon neutrality |

| BMW | All-EVs should account for about 50% of their deliveries | - | - | Carbon neutrality |

| Honda | EVs and FCEVs represent 40% of its global auto sales | - | EVs and FCEVs represent 100% of its global vehicle sales | Stop ICE vehicle sales |

| Ford | 50% of Ford’s global vehicle sales volume is expected to be electric | - | - | |

| Mitsubishi | - | 100% electrified sales | - | |

| Suzuki | 80% BEV sales in Europe | - | - |

Before 2030

Before 2035

Before 2040

Before 2050

Lithium

Lithium: Essential for Green Energy

Lithium, the lightest metal on Earth, is indispensable for the future of clean energy. Although it constitutes just 0.002 percent of the Earth’s crust, lithium’s unique properties make it essential for the energy storage solutions that underpin the global transition to renewable energy and electric vehicles. The largest lithium concentrations can be found in granitic pegmatites and continental brines.

Critical Role in the Green Energy Transition

The shift to clean energy technologies requires a significant increase in the use of critical minerals compared to fossil-fuel-based counterparts, with lithium at the forefront.

The ability to store energy is crucial for the green energy transition. The combination of low weight and high energy storage density makes lithium the perfect material for batteries. As the world moves away from fossil fuels, the demand for lithium will continue to soar, making it a critical material in the fight against climate change.

Securing a Sustainable Future with Abundant Resources

The importance of lithium has been recognized by major economies, with the U.S. and Europe designating it as a critical raw material vital for economic and technological stability.

Fortunately, global lithium reserves are ample and, with responsible and innovative extraction practices, can meet the growing demand. This abundance ensures that lithium will play a central role in supporting the green energy transition, enabling a sustainable and resilient future for future generations.

Lithium Extraction Technologies

Lithium Production Technologies

Comparison of conventional lithium extraction technologies.

DLE from Brine |

Solar Evaporation Brine Extraction |

Hard Rock Mining |

|

|---|---|---|---|

| Feedstock | Continental brine | Continental brine | Rock / spodumene |

| Project implementation time | 5-7 years | 13-15 years | 8-10 years |

| Lithium carbonate production time | 2 hours | 2-3 years | 3-6 months |

| Lithium yield | 80-95% | 20-40% | 6-7% |

| Average footprint per 1,000 mt LCE | 1.4 acres | 65 acres | 115 acres |

| System design | Mobile / stationary | Stationary | Stationary |

| Environmental impact | Minimal | Soil- and water contamination | Soil- and water contamination |

| Water consumption per 1,000 mt LCE | 80 million gallons | 550 million gallons | 250 million gallons |

| CO₂ footprint per 1,000 mt LCE | 1.5 million kg | 5 million kg | 15 million kg |

| Average invested capital per 1,000 mt LCE | $45 million | $50 million | $60 million |

| Average cost per metric ton | $5,700 | $5,800 | $6,900 |

DLE from Brine

Solar Evaporation Brine Extraction

Hard Rock Mining

Direct Lithium Extraction from Brine

Please have a look at traditional direct lithium extraction from brine.

Direct Lithium Extraction (DLE) represents a transformative approach to lithium extraction, offering numerous advantages over traditional methods. DLE technologies can be classified into adsorption, ion exchange, and solvent extraction processes. These innovative techniques enable lithium extraction directly from complex brines with high concentrations of various ions.

Solar Evaporation Brine Extraction

Please have a look at traditional lithium extraction from solar evaporation brine.

Solar evaporative brine processing has been a dominant method for lithium extraction, particularly in South America's Salars. Solar evaporation is commonly employed in lithium extraction from brine and relies on solar evaporation to concentrate lithium and other salts. The brine is pumped into expansive evaporation ponds, occupying vast areas, where it undergoes a year-long process to achieve sufficient lithium concentration. However, this method presents several concerns:

- It consumes an immense amount of water, further straining regions already facing water scarcity.

- The recovery rates are relatively low, typically capturing only about 50% of the original lithium content of the brine.

- The disposal of waste salts and the use of chemical reagents pose environmental challenges.

Hard Rock Mining

Please have a look at traditional lithium extraction from hard rock mining.

Hard rock mining, focusing on extracting lithium from spodumene-bearing pegmatites (or clusters of rocks and crystals), involves energy-intensive processes and chemical usage. After mining the ore, it undergoes crushing, concentration, and chemical treatments, including roasting and leaching, to obtain a lithium concentrate. This method poses several environmental concerns, such as chemical waste disposal and groundwater contamination, rivers, and soil contamination. The transportation of crushed rock to China for processing adds to the carbon footprint and the need for more transparency regarding waste handling practices.

We Turn Wastewater Into High-Value Minerals

Our Solution

Sustainable lithium extraction from oilfield wastewater with pioneering process for DLE combined with advanced water treatment solutions.

Lithium Harvest is pioneering a future where environmental stewardship and industrial progress converge. Our proprietary and patented solution efficiently transforms oilfield wastewater into high-purity, battery-grade lithium compounds, revolutionizing lithium extraction. By employing Direct Lithium Extraction (DLE) combined with advanced water treatment, we achieve production in just two hours - a stark contrast to the years-long processes of traditional methods.

Our agile and modular facilities, strategically co-located with midstream operators, drastically shrink operational footprints by up to 99% and slash capital expenditures by up to 70% compared to traditional mining. We do extraction and refining in decentralized facilities. Operating directly on the feedstock suppliers' land, we maintain a minimal environmental impact, safeguard wildlife, and offer beneficial reuse options.

In the burgeoning markets for electric vehicles and batteries, Lithium Harvest stands as a beacon of sustainable extraction, demonstrating

that high-value minerals can be responsibly sourced.

We believe that our patented technology is the fastest to market and lowest cost of any lithium mining technology in the market.

Direct Lithium Extraction - But Different

Our patented technology is Direct Lithium Extraction (DLE) based on adsorption technology. Using wastewater from oil & gas production as our feedstock allows us to bring lithium operations online much quicker and at a lower cost than any other DLE technology in the market.

Lithium Harvest Solution |

DLE from Brine |

Lithium Harvest Advantage |

|

|---|---|---|---|

| Feedstock | Produced water | Continental brine | No drilling permits needed |

| Project implementation time | 12-15 months | 5-7 years | No asset acquisition |

| System design | Modular and mobile | Mobile / stationary | Unique modular design |

| Water consumption | 20 million gallons | 80 million gallons | Water recycled for secondary reuse |

| CO₂ footprint | Neutral | 1.5 million kg | Offsets CO₂ footprint from wastewater |

| Average invested capital per 1,000 mt LCE | $18 million | $45 million | No land acquisition |

| Average cost per metric ton | $4,550 | $5,700 | Low energy technology |

Lithium Harvest Solution

DLE from Brine

Lithium Harvest Advantage

Lithium Harvest vs. Traditional Lithium Mining

Technology Benchmark - Environmental Impact

Zero-Carbon Footprint

Our innovative method eliminates the necessity for transporting materials to separate refining locations. Our low-pressure, energy-efficient process also relies on solar energy as the primary power source, diminishing our environmental impact. We use electricity in our production, which creates a carbon footprint. However, when we offset that against the carbon emissions saved in the oilfield wastewater disposal, we are actually carbon neutral. We save up to 15 million kg of CO₂ emitted by traditional lithium mining per 1,000 metric tons of lithium carbonate produced.

Compact Facility Design: Eco-Conscious Operations

Our dedication to environmental stewardship is evident in the design of our facilities. Lithium Harvest’s operations are strategically located alongside produced water treatment centers. Our facilities are modular and compact, designed for easy integration and quick deployment without large ponds or extensive pipelines like conventional extraction technologies. This strategy not only conserves space but also safeguards the local environment and wildlife, preventing any extra ecological disruption.

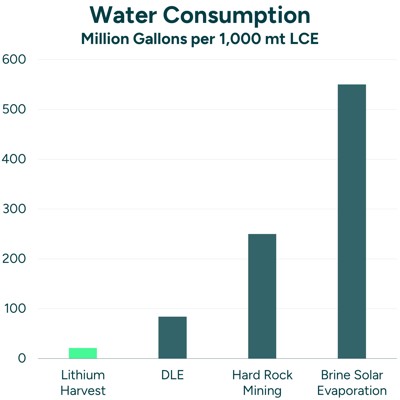

Minimal Water Consumption

We use minimal freshwater in our production process. In fact, we can even clean the oilfield wastewater after the lithium extraction process and use it for secondary reuse. Our extraction process recycles more than 90% of the water and does not generate any waste by-products, reflecting our commitment to protecting the Earth’s vital water resources. We save up to 96% of the water used in traditional lithium mining, which equals more than 500 million gallons of water per 1,000 metric tons of lithium carbonate produced.

Technology Benchmark - Business Case

Optimized Capital Expenditure

We’ve streamlined the initial investment in lithium extraction infrastructure. By eliminating the need for land acquisition and drilling rights, we’ve significantly reduced CapEx. Our modular plant design is cost-effective and allows for rapid deployment and expansion, easily fitting into various operational scales.

Cost Leadership in Lithium Production

We have achieved a breakthrough in cost-reduction in lithium compound production. Our technology delivers up to 95% yield, and our fully automated, low-energy facility ensures efficiency at every stage. Our on-site production and refining processes, alongside fixed-price feedstock agreements, allow us to offer lithium compounds at costs that are up to 35% lower than traditional mining methods, positioning us as a leader in cost competitiveness.

Accelerating Project Timelines

We’ve transformed the timeline for bringing new lithium operations online. Traditional mining operations can take up to 15 years to reach full production, but our innovative approach - leveraging existing oilfields - sidesteps the need for drilling permits. As a result, we can establish operations in just one year, a game-changing pace that reduces market entry risks. This agility in production scaling lets us rapidly meet increasing customer demands, propelling Lithium Harvest to the forefront of the industry.

The Environmental Impact of EVs - and How We Make It Even Cleaner

How EVs Reduce Environmental Impact

Electric vehicles (EVs) are revolutionizing transportation by significantly reducing environmental impacts, particularly greenhouse gas (GHG) emissions. According to recent studies from IEA, the switch from internal combustion engine (ICE) vehicles to EVs is projected to avoid a staggering 2.6 gigatonnes of CO₂ by 2035 globally.

In the U.S. alone, battery electric vehicles (BEVs) today demonstrate lifecycle emissions that are 45%-65% lower than those of plug-in hybrid electric vehicles (PHEVs), hybrid electric vehicles (HEVs), and ICE vehicles. Over a medium-sized BEV’s lifetime, this translates to an estimated 50 tonnes of CO₂-equivalent savings.

However, the true environmental impact of EVs extends beyond their operational emissions. The production of EV batteries, particularly lithium-ion batteries, remains a significant source of emissions. As a result, the global community continues to seek ways to enhance the sustainability of EVs, focusing on reducing the carbon footprint associated with battery production and critical mineral extraction.

And We Can Make It Even Cleaner

Lithium Harvest is at the forefront of making EVs even greener. Our patented solution, which responsibly extracts lithium from oilfield wastewater, is poised to slash up to 47% of battery lifecycle emissions. This advancement not only accelerates the environmental breakeven point of EVs, reducing it from 18,000 km to just 6,000 km, but it also brings substantial water and land conservation benefits - saving approximately 15-20 cubic meters of water and freeing up 50-100 square meters of land per EV produced.

As the global shift towards electrification continues, with EVs expected to comprise half of all car sales by 2035, the importance of sustainable battery manufacturing and critical mineral extraction cannot be overstated.

The Lithium Market

The World is Facing a Lithium Shortage

As the global shift towards green energy accelerates, the demand for lithium has surged to unprecedented levels. Between 2023 and 2030, lithium demand is projected to increase 3.5 times, driven by the rapid adoption of EVs and lithium-ion batteries. This surge underscores the urgency for sustainable lithium to meet the growing needs of a decarbonizing world.

The industry is on the brink of a severe supply shortfall despite increased lithium production. By 2029, global lithium demand is expected to outstrip supply, potentially leading to a critical shortage that could destabilize markets and hinder the green energy transition. To put this into perspective, more lithium will be needed in 2029 alone than was mined globally between 2015 and 2022. Projections indicate that by 2034, the demand for lithium could be 6.5 times greater than in 2023, further exacerbating the supply gap.

The World Needs More Sustainable Lithium

The lithium surge has not only highlighted the critical importance of lithium but also underscored the urgent need for more sustainable extraction methods. Traditional lithium mining practices, such as open-pit mining and brine evaporation, are associated with significant environmental concerns, including water depletion, soil degradation, and high carbon emissions. Recognizing these challenges, industries and governments worldwide are turning their focus towards sustainable lithium.

The push for sustainable lithium is not just an environmental imperative but also a business one. Major players in the EV and tech industries, conscious of their carbon footprint and eager to appeal to environmentally aware consumers, are increasingly seeking responsibly sourced lithium - on both the buy and sell sides, sustainability is now a critical metric when supply agreements are being discussed. Benchmark Minerals, a leader in commodity price assessment and market intelligence, has developed a forecasted global mined lithium production by Benchmark ESG Tier. This forecast demonstrates a significant surge in the supply of sustainable lithium, underscoring an even higher potential if the world is transitioning to more sustainable lithium products.

The Imperative for Sustainable Lithium: A Global Necessity that Cannot Be Ignored

- Environmental Concerns: Traditional mining methods, such as open-pit mines and brine evaporation, pose serious environmental threats.

- Sustainable Shift: The industry and governments are pursuing sustainable lithium extraction techniques to mitigate these impacts.

- Sustainability as a Metric: Major EV and tech companies prioritize responsibly sourced lithium, influencing supply agreements.

- Strategic Advantage: Companies capable of supplying sustainable lithium are setting the pace for a greener future and carving out a competitive edge in a market at the cusp of transformation.

Future Projections Highlight the Urgency and Potential Impact

The push for sustainable lithium is not just a matter of environmental responsibility but a response to the stark realities of future supply and demand. Projections indicate that as the adoption of sustainable lithium grows, the high-case scenario could result in a significant supply shortage - nearly 10 million tons of lithium carbonate equivalent (LCE) between 2025 and 2034. Even in a base-case scenario, the supply gap will be almost 2.5 times larger by 2034. To meet the high-case demand in 2034, the world will need over 1 million additional tons of LCE sourced through sustainable methods.

The Lithium Market

Geography

Today, about 90% of all lithium is produced in Australia, Chile, China, and Argentina. Australia is the largest lithium producer, making over 40% of all lithium in 2022. However, most of the ore from Australia is processed in China, which ultimately controls the refined product.

Lithium Sources

In 2024, 66% of lithium came from ore mining and 34% from brine extraction. Simply put, Australia’s lithium comes from ore mining, whereas Chile and Argentina rely on continental brines.

U.S. Production

U.S. lithium production is down from 27% of the global production in 1996 to less than 1% in 2023. As highlighted in the Inflation Reduction Act, it is critical for the U.S. to become self-sufficient with lithium.

End-Use Markets

The surge in EV and battery adoption is the primary driver of current lithium demand, accounting for 87% of output in 2024. However, lithium is used in many end markets, including batteries for consumer electronics, air treatment, ceramics, glass, greases, and casting powder.

It's important to identify lithium resources in the U.S. so that our supply does not rely on single companies or countries in a way that makes us subject to economic or political manipulation.

Global Battery Gigafactory Capacity: A New Lithium Deficit?

Massive investments and growth in lithium-ion batteries.

As lithium-ion batteries increasingly dominate global lithium consumption, the demand for battery capacity is set to increase drastically. Current projections indicate that global battery capacity will expand from just over 2 TWh in 2023 to more than 8 TWh by 2030 - a fourfold increase within a decade.

To bridge the gap between the existing battery industry and the anticipated demand by 2040, an investment of at least $1.6 trillion will be necessary across the entire supply chain. This figure represents nearly three times the $571 billion required to meet demand by 2030.

According to Benchmark’s Lithium-ion Battery Database, battery demand is expected to double again between 2030 and 2040, underscoring the scale of the challenge ahead. Of the $1.6 trillion required by 2040, 44% will be allocated to the construction of battery gigafactories, which are critical for the mass production of battery cells and the assembly of battery packs. These gigafactories are essential to meet the growing demand driven by the rapid adoption of electric vehicles, energy storage systems, and other advanced technologies reliant on lithium-ion batteries.

These investment estimates are based on Benchmark’s base case scenario, reflecting current trends and realistic growth projections. However, if the ambitious targets set by policymakers, industry leaders, and environmental advocates are to be met - such as achieving net-zero emissions by 2050 or fully transitioning to renewable energy sources - the required investment could escalate significantly. This underscores the importance of strategic investments, innovation in battery technology, and the development of sustainable supply chains to ensure that the battery industry can keep pace with global decarbonization efforts.

Rapid Growth of U.S. Demand and Battery Manufacturing

The U.S. battery manufacturing sector is poised for unprecedented growth, driven by the surge in demand for electric vehicles (EVs) and the broader transition to renewable energy. Legislative support, particularly from the Inflation Reduction Act, has accelerated the development of the E.V. supply chain.

By 2025, U.S. battery manufacturing capacity is expected to reach 440 GWh, a significant leap from the current 119 GWh. This growth trajectory is set to continue, with projections indicating a capacity of over 1000 GWh by 2030 - an almost ninefold increase from today’s production. Such growth is set to impact both local and global lithium supply chains, reflecting the critical importance of expanding lithium production and refining capabilities within the U.S.

Increasing Demand for Raw Materials

The rapid expansion of the battery manufacturing industry has intensified the competition for locally sourced raw materials. By 2025, the U.S. demand for critical raw materials (CRMs) such as lithium is anticipated to be 10x higher than the planned refining capacity, highlighting a significant supply gap that must be addressed. Analysts forecast a 487% increase in U.S. lithium demand by 2030, underscoring the urgency for a robust domestic supply chain to support the growing number of giga-factories—currently estimated at over 47 nationwide.

The Imperative of Domestic Production

The strategic importance of domestic lithium production cannot be overstated. Beyond supporting the rapid expansion of battery manufacturing, domestic production is essential for sustaining U.S. economic growth, enhancing competitiveness, and ensuring energy independence. As the demand for lithium carbonate equivalent (LCE) reaches an estimated 750,000 mt by 2030, domestic production will play a pivotal role in meeting this demand, creating high-quality jobs and local growth.

National Security and Supply Chain Resilience

The U.S. government’s strategic initiatives to reduce reliance on imports, particularly from geopolitical adversaries, are crucial in mitigating supply chain risks and ensuring the resilience of the E.V. industry. By bolstering domestic production capabilities, the U.S. can safeguard against global supply disruptions.

Government Support and Strategic Initiatives

The U.S. government has recognized the strategic importance of the lithium supply chain through various grants, subsidies, and tax incentives. The Inflation Reduction Act is a key driver, offering substantial support to domestic producers and manufacturers.

Lithium Price Dynamics & Future Outlook

The lithium market has experienced volatility over recent years, driven by a combination of supply-demand imbalances, geopolitical factors, and global economic events. After peaking at record highs of over $80,000 per tonne in 2022, lithium prices saw a correction in 2023 due to oversupply and a slowdown in demand from the battery and EV sectors. However, this price drop is a short-term phenomenon, as the underlying fundamentals of the lithium market remain strong.

Price Drivers and Market Dynamics

- Supply and Demand Imbalances: The temporary oversupply in 2023 led to price volatility, but with demand for lithium continuing to grow, particularly from the EV and battery sectors, prices are expected to stabilize. The market is navigating a delicate balance, with new projects potentially expanding global lithium carbonate equivalent (LCE) capacity. However, the commissioning of these projects is at risk, including potential delays/cuts and rising production costs.

- Geopolitical Factors: China’s dominance in the lithium-ion battery market has introduced significant supply chain vulnerabilities. China holds approximately 7% of the world’s lithium resources but controls over 70% of the supply chain. This concentration has prompted other countries to consider strategic stockpiling and investments in domestic lithium production to mitigate risks.

- Global Economic and Political Events: Economic factors such as inflation, the ongoing Ukraine war, and subsidies for clean energy and EV adoption have also played a crucial role in shaping the lithium market. These factors continue to influence global energy markets, with potential ripple effects on lithium demand and pricing.

Lithium Price Projections

- Short-Term Price Outlook: Lithium prices are projected to stabilize from $15,000 to $20,000 per tonne by the second half of 2025. The demand for sustainably sourced lithium is on the rise, driven by corporate and governmental incentives, which could lead to a premium pricing scenario for lithium products that are responsibly sourced.

- Long-Term Price Outlook: Benchmark’s long-term forecast suggests lithium carbonate prices could reach around $30,000 per tonne. This increase is supported by future imbalance and the anticipated introduction of regulated commodity futures for lithium, which would contribute to greater price stability and predictability. The continued growth in EV adoption and battery manufacturing will further tighten the supply-demand balance, potentially driving prices upward.

Analyst Price Forecast

2025 |

2026 |

2027 |

2028 |

|

|---|---|---|---|---|

| Benchmark Mineral Intelligence | $16,362 | $18,200 | $22,000 | $27,300 |

| Fastmarkets | $16,250 | $16,250 | $18,500 | $20,000 |

| S&P Global | $15,700 | $16,300 | $18,000 | $21,250 |

2025

2026

2027

2028

Growing Offtake Markets

- Projected EV sales in 2024: ~17 million units

- In 2024, EVs will account for over 20% of global car sales

- If 1 million more EVs were sold, approx. 53,125 mt of LCE would be needed

Sales Growth:

- H1 2024: 7 million EVs sold

- 20% increase from H1 2023

Battery Demand:

- Global battery demand in 2024: 512 GWh

- 23% year-on-year growth

- Sustained growth trend expected to remain

Future Projections:

- By 2035, 50% of all cars sold globally will be electric

- The global EV fleet is projected to grow twelve-fold to 585 million by 2035, with an average annual growth of 24% from 2023 to 2035.

Manufacturer Commitments:

- 20+ major car manufacturers (90% of global car sales in 2023) have electrification targets

Market Trends:

- Increasing availability of EVs, particularly larger ones

- The average size of lithium-ion battery packs in EVs is growing by ~10% annually

Raw Material Demand:

- Increasing need for critical raw materials: lithium, cobalt, and nickel due to more battery production

The World's Most Sustainable Lithium

Corporate Presentation

-

Unveiling the Future: Discover how Lithium Harvest is poised to shape the energy industry's future with our innovative technology and solution.

-

Driving the Green Energy Revolution: Explore the vital role of lithium in driving the global green energy transition and how Lithium Harvest is at the forefront of this transformation.

-

Seizing Market Opportunities: Gain insights into the current market situation, technology benchmarking, and vast market opportunities.

Please see our corporate presentation from December 2024.

Download PDF, 3.50 MBCorporate Contact

-

Sune Mathiesen

- Chairman & CEO

- +1 713 887 0751

- sma@lithiumharvest.com